High Value Insurance and Signature Services

High value shipments create asymmetric risk. One lost box and a month of margin disappears. The High Value Insurance and Signature Services Hub lays out how coverage and delivery controls actually work so you can pick the right mix, budget for it, and avoid denials or repeat losses. If you ship jewelry, electronics, collectibles, or high-ticket B2B goods, small choices around insurance and signature services move real money.

The core idea is simple, but easy to miss. Carrier liability, declared value coverage, and third-party insurance are different products with different rules. Understanding those differences is the single best step an ops lead can take before sending valuable items. Pair that with the right signature level or controlled pickup, and you convert theft and damage from existential risk into a managed cost.

High Value Insurance, Liability, And Third-party Coverage#

Every shipment sits on a coverage stack. One layer is automatic, the rest are optional. They do not pay out the same way or for the same reasons.

At a glance:

| Coverage type | Who provides it | What it is | Typical limits and gaps | Cost pattern | Claims reality |

|---|---|---|---|---|---|

| Carrier liability | The parcel or LTL carrier | Baseline responsibility if the carrier is negligent | Often limited by service guide, commodity, or per-pound schedules for LTL. Exclusions are broad | Included, but payouts capped by tariff and proof hurdles | Must show carrier fault. Packaging or documentation issues sink many claims |

| Declared value coverage | The parcel carrier as an add-on | You declare a value, pay a fee, carrier increases its maximum liability | Still subject to carrier terms and packaging standards. Not full insurance | Fee scales with declared amount | Faster than liability-only, but denials still common on packaging or concealed damage |

| Third-party cargo insurance | Independent insurer via broker or platform | True insurance that targets full invoice value and stated perils | Policy-specific exclusions apply, but usually broader than carrier terms | Often a percent of value quoted upfront | Separate claim process, can be cleaner and more predictable if documentation is solid |

Why carriers separate these layers: liability is about their negligence standard and tariff rules, not making you whole. Declared value recoups carrier risk with a per-value fee. Third-party insurance prices the actual exposure and sits outside carrier adjudication.

For LTL, the gap is bigger. Default carrier liability is frequently a published per-pound limit by freight class, which rarely covers full value. Full-value cargo insurance bought through a third party is a different promise with different triggers.

Carrier liability vs cargo insurance

Signature And Delivery Control Services#

Insurance only pays after loss. Signature services and controlled delivery reduce loss events in the first place. Carriers offer several signature tiers. With parcel networks you can choose options where someone at the address signs, the named recipient must sign, or an adult must sign with age verification. FedEx publishes four signature options. UPS and USPS offer their own tiers with similar ideas.

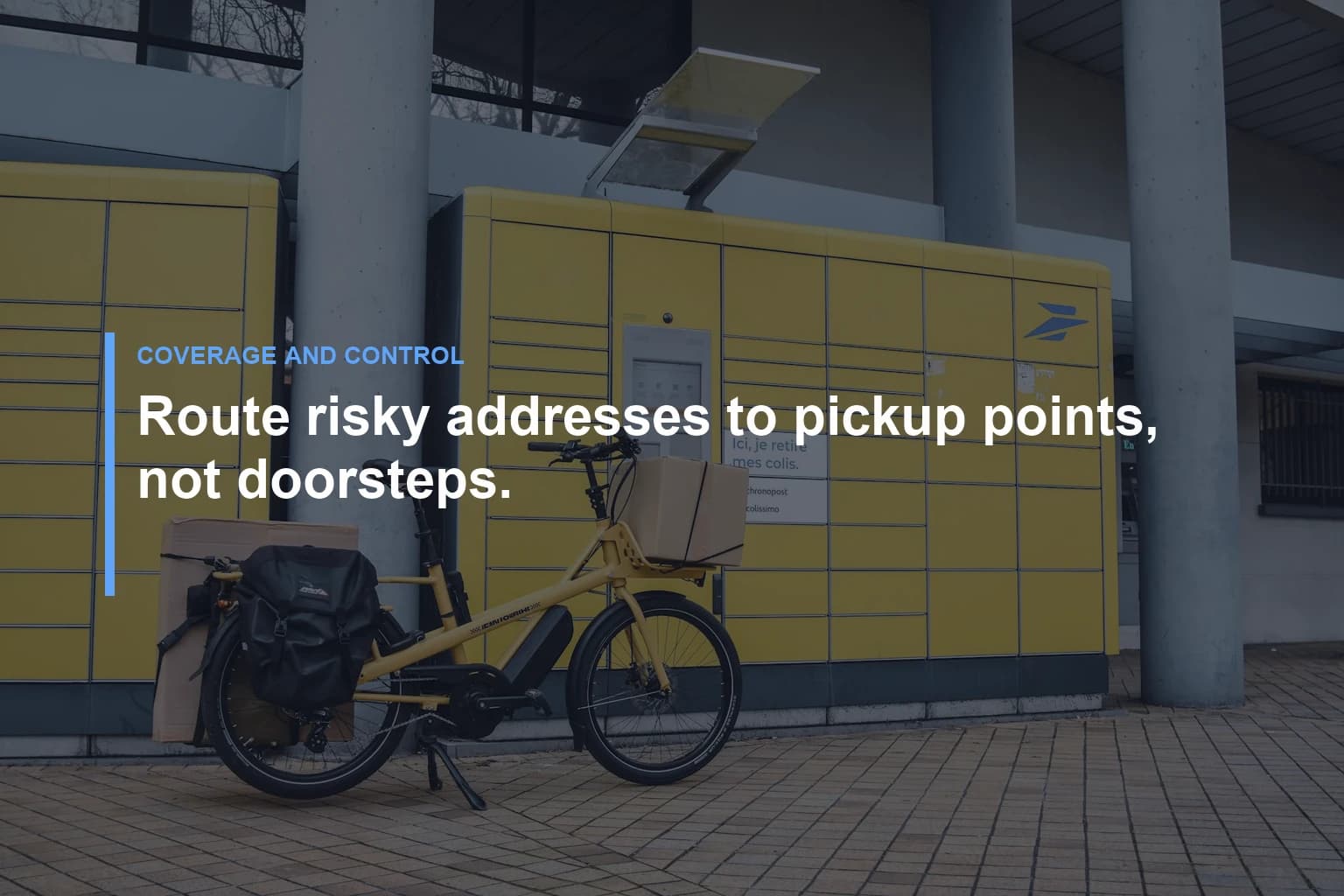

Two operational levers matter here. Signature level and delivery location. A signature adds cost and can slow a route. But it shuts down the most common porch-theft scenario. Delivery to a staffed pickup point cuts risk further. A delivery access point gives the carrier a secure site to deliver your package for customer pickup, instead of leaving it at a doorstep.

delivery access point

Use signature where the loss pattern justifies it. Use access points for high-density theft zip codes, high-value consumer orders, or addresses that frequently result in claims or chargebacks.

How To Decide What To Buy And When#

You do not need every control on every order. Match spend to exposure.

Two questions get you 80 percent of the way:

- If this parcel disappears or arrives damaged, what is the net financial hit after margin and chargeback risk?

- Is the route, destination, or product type prone to theft or concealed damage?

Then layer controls:

- For modest value items with low theft risk, rely on carrier liability or limited declared value and drop signature.

- For high value items where doorstep risk is high, pair third-party insurance with adult or direct signature, or require pickup.

- For LTL with fragile or expensive freight, buy third-party cargo insurance and crate or palletize to specification, then require delivery appointment with signature.

Cost context helps. Third-party parcel insurance sold through shipping platforms is often priced around 1 percent of the declared value, while carrier-provided declared value rates trend closer to 3 percent of value according to business sources. Rates vary by provider and commodity. Compare real quotes for your lanes and items, not list anecdotes.

Third-party shipping insurance vs. declared value

Incoterms And International Risk Transfer#

Export terms decide who owns risk, who buys insurance, and who deals with the carrier. Incoterms are 11 standardized rules that assign responsibilities between seller and buyer. That includes transport, insurance, customs clearance, and the exact point where risk transfers.

Incoterms

Pick the rule that matches your control and customer promise. If you sell Delivered Duty Paid, you own transport risk to the buyer’s door, so you decide the insurance and signature level. If you sell Ex Works or FCA and the buyer controls main carriage, your risk likely ends earlier and their policy governs. Misaligned terms lead to unpaid claims and angry customers. Align product value, route risk, and Incoterms before quoting.

Practical Setup And Evidence That Wins Claims#

Controls only work if your process supports them. Carriers and insurers look for consistent packaging, clear value proof, and traceable chain of custody.

Build a simple playbook:

- Standardize packaging by product family, including internal immobilization and corner protection for heavy items.

- Capture proof up front. Photograph packed contents and outer box for high value parcels, keep serials or IMEIs, and invoice copies.

- Print readable labels, avoid covering seams with tape, and keep barcodes flat. Mis-scans drive “lost in building” outcomes.

- Choose signature level and pickup vs doorstep based on a ZIP and value matrix in your OMS, not one-off judgment.

Document everything that touches the parcel. If a claim happens, you need invoice value, shipment details, delivery scan history, and photos. Third-party insurers often adjudicate faster when documentation is complete on first submission. Carrier declared value claims tend to test packaging compliance closely, so front-load that proof.

Common Traps That Create Avoidable Loss#

The patterns repeat. Fix them once.

- Declaring a high value but skipping the add-on fee, then assuming “it was insured.” Declared value only changes payout if you bought it.

- Buying declared value coverage, then shipping in packaging that does not meet carrier standards. That invites denial on damage.

- Requiring adult signature on every order, including low-risk, low-value shipments. You pay surcharge and increase failed delivery without reducing meaningful risk.

- Shipping expensive goods to chronic porch-theft neighborhoods with no delivery controls. Use access points or hold-for-pickup by default for those ZIPs.

Budgeting And Measurement#

Treat insurance and signature as a controllable cost center. Track three numbers by product group and destination type: spend on coverage and delivery controls, claim recoveries, and preventable losses. If controls cost less than the avoided losses plus improved recovery, keep them. If not, change the mix.

Start with a pilot on the riskiest quadrant, for example, consumer orders over a defined value to theft-prone ZIPs. Add adult or direct signature and third-party insurance. Monitor chargebacks and claims. If loss events drop and recovery improves, expand. If customer experience takes a hit, pivot to pickup locations or delivery windows that reduce missed attempts.

The system is mechanical. Know what each coverage layer promises, pick the least-cost control that blocks the loss you are seeing, and keep the paperwork needed to get paid when things still go wrong.

Shipping insurance for high-value items